Fed Chair Jay Powell recently revealed that he gets advance notice of economic releases that could shape the direction of Fed policy…

I suspect the employment report coming out at 8:30 a.m. today is one of those releases.

Ever since his Senate testimony on March 7, the market no longer assumes that the March 22 meeting will result in a mere 25 basis point (bps) hike…

Now the market is pricing in the very real possibility of 50 bps…

Here’s Powell’s statement on Tuesday that caused the shift…

Multiple key data points remain to be released ahead of the March 22 meeting, and we therefore continue to expect a 25 bps increase but are likely [going] to add another quarter-point hike to our estimate of terminal to bring it up to 5.5%, should we see reasonable strength in Friday’s payrolls and wages.

Almost instantly, the Fed Fund swap market took what he said to heart…

Here’s the swap curve before the meeting compared to where it is now…

They think that a surprise hike is more likely to happen now rather than later.

Needless to say, the yield curve legged down on the news to get almost obscenely inverted.

Powell was hawkish at that meeting – really hawkish…

Maybe he reads our newsletter… Just last week, we remarked on the market’s non-reaction to the latest economic data. We said, “Markets saw no evil and heard no evil… in this case, about the need to keep rates higher for longer – and probably more than expected.”

Compare that to what Powell said this week…

The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.

In fact, he was so hawkish, he had to walk back his comments the very next day right before his second round of testimony.

When Fed officials tell you they don’t care about market reactions… don’t believe them. Because they do. Powell’s walk-back seemed like a sign of weakness coming… or at least a lack of intestinal fortitude. The problem is he’s still hoping for a soft landing… hence the kowtowing.

It’s probably a sign of the times…

Back in the ’80s when Volcker righted the inflation ship, he just did what he had to do, come what may. There wasn’t this dual target of fighting inflation and keeping the stock market up. His vision saw farther.

What’s alarming is that Fed Fund swaps have been predicting what will happen to rates since the market started falling in January 2022…

The market knew what the Fed would do… and when it would do it… before the Fed itself did…

Not a great look for the economists trying to lead us out of inflation.

Free Trading Resources

Have you checked out Larry’s free trading resources on his website? It contains a full trading glossary to help kickstart your trading career – at zero cost to you. Just click here to check it out.

Of course, it’s not a guarantee that the Fed will lift rates by 50 bps during the March meeting. They may go ahead with 25 bps and kick the additional 25 bps down the road to a future meeting.

But if today’s jobs report and the consumer price index (CPI) report next Tuesday don’t support the Fed’s “early stages of disinflation” narrative… then it will almost certainly be 50 bps.

It’s hard to imagine today’s jobs report will be soft, though. The Job Openings and Labor Turnover Survey (JOLTS) job openings on March 8 showed 10,824 compared with 10,546 estimates.

Before the last monster jobs report came out on February 1, the preceding JOLTS report showed 11,012 which obliterated expectations by more than 700. Two days later, the monthly employment report was one of the biggest month-over-month increases in history.

And as far as the CPI report goes, falling commodity prices have already been absorbed by the data. Commodities have been rather flat lately… so the burden of reducing inflation will fall on services and the cost of shelter.

Meanwhile, the Nasdaq 100 – which is supposed to be sensitive to big changes in interest rate expectations – has been stuck in a range over the last month. And it completely obliterated the performance of both the Dow Jones (DIA) and SPDR S&P 500 ETF Trust (SPY).

I suspect that strength is coming from retail favorites holding up the fort… like NVIDIA (NVDA), something we spoke about last week. The key level to watch there is $227 – its trailing 20-day volume-weighted average price (VWAP).

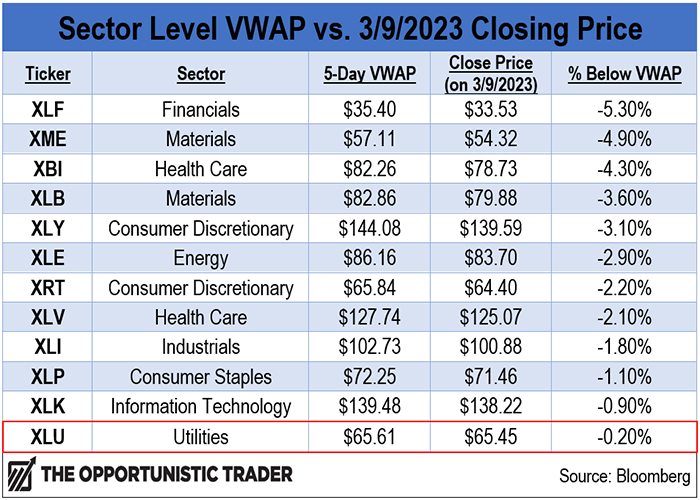

But once you fly above the noise, sector performance is telling a different story.

Take a look at where key sectors are trading relative to their 5-day VWAP.

The only sector that’s at least somewhat holding up around its 5-day VWAP is the Utilities Select Sector SPDR Fund (XLU). Sector performance has leaned extremely defensive.

When XLU starts holding up compared to sectors that fly high in a bull market, it’s usually not a great sign.

Investors flock to XLU when they want stable cash flows… not when they’re bullish on the economy.

All of this feels eerily similar to the highs last summer… after the Nasdaq ran up over 20% and a new bull market was declared. The patients had taken over the insane asylum…

So these two upcoming reports are important…

Because if stock prices correct due to stronger-than-anticipated jobs and CPI data… it might snowball into something more.

Regards,

Eric Shamilov

Analyst, Trading With Larry Benedict

P.S. Did you catch Larry’s Shockwave Summit on Wednesday night? If not, there’s only a little bit more time before Larry issues his big trade.

The last time he issued a shockwave trade, you could have made 175% in less than a day. But only if you were ready before the shockwave hit. To learn more, catch the replay here.

By how many basis points do you think the Fed will increase our next rate hike?

Let us know your thoughts – and any questions you have – at feedback@opportunistictrader.com.

Reading Trading With Larry Benedict will allow you to take a look into the mind of one of the market’s greatest traders. You’ll be able to recognize and take advantage of trends in the market in no time.